Motivation for reading / Who should read this:

I read Validity and Validation – Understanding Statistics, by Catherine S. Taylor in part as a follow up to the meta-analysis book from two weeks ago, and in part because I wanted to know more about the process of validating a scale made from a series of questions (e.g. The Beck Depression Inventory, or a questionnaire about learning preferences). For scale validation, there’s a field called Item Response Theory, which I understand better because of this book, but not at any depth.

This book, a quick read at 200 small pages, compliments the handbook of educational research design that Greg Hum and I made. I plan to recommend it anyone new to conducting social science research because it provides a solid first look at the sort of issues that can prevent justifiable inferences (called “threats to internal validity”), and those that can limit the scope of the results (called “threats to external validity”).

A good pairing with “Validity and Validation” is “How to Ask Survey Questions” by Ardene Fink. My findings from that book are in this post from last year. If I were to give reading homework to consulting clients, I would frequently assign both of these books.

What I learned:

Some new vocabulary and keywords.

For investigating causality, there is a qualitative analogue to directed acyclic graphs (DAGs), called ‘nomological networks’. Nomological networks are graphs describing factors, directly or not, that contribute to a construct. A construct is like a qualitative analogue of a response variable, but has a more inclusive definition.

To paraphrase of Chapter 1 of [1], beyond statistical checks that scores from a questionnaire or test accurately measure a construct, it’s still necessary to ensure the relevance and utility of that construct.

Hierarchical linear models (HLMs) resemble random effect models, or a model that uses Bayesian hyperpriors. An HLM is a linear model where the regression coefficients are themselves response values to their own linear models, possibly with random effects. More than two layers are possible, in which the coefficients in each of those models could also be responses to their own models, hence the term ‘hierarchical’.

What is Item Response Theory?

Item response theory (IRT) is set of methods that puts both questions/items and respondents/examinees in the same or related parameter spaces.

The simplest model is a 1-Parameter IRT model, also called a Rasch model. A Rasch model assigns a ‘difficulty’ or ‘location’ for an item based on how many respondents give a correct/high answer or an incorrect/low answer. At the same time, respondents also have a location value based on the items they give a correct/high response. An item that few people get correct will have a high location value, and a person that gets many items correct will have a high location value.

A 2-parameter model includes a dimension for ‘discrimination’. Items with higher discrimination will elicit a greater difference in responses between respondents with a lower and those with a higher location than the item. Models with more parameters and ones for non-binary questions also exist.

The WINSTEPS software package for item response theory (IRT):

WINSTEPS is a program that, when used on a data set of n cases giving numerical responses each of to p items, gives an assessment of how well each item fits in with the rest of the questionnaire. It gives two statistics: INFIT and OUTFIT. OUTFIT is like a goodness-of-fit measure for extreme respondents at the tail-ends of dataset. INFIT is a goodness-of-fit measure for typical respondents.

In the language of IRT, this means INFIT is sensitive to odd patterns from respondents whose locations are near that of the item, and OUTFIT is sensitive to odd patterns from respondents with locations far from the item. Here is a page with the computations behind each statistic.

On CRAN there is a package called Rwinsteps, which allows you to call functions in the WINSTEPS program inside R. There are many item response theory packages in R, but the more general ones appear to be “cacIRT”, “classify”, “emIRT”, “irtoys”, “irtProb”, “lordif”, “mcIRT”, “mirt”, “MLCIRTwithin”, “pcIRT”, and “sirt”.

For future reference.

Page 11 has a list of common threats to internal validity.

Pages 91-95 have a table of possible validity claims (e.g. “Scores can be used to make inferences”), which are broken down into specific arguments (e.g. “Scoring rules are applied consistently”), which in turn are broken down into tests of that argument (e.g. “Check conversion of ratings to score”).

Pages 158-160 have a table of guidelines for making surveys translatable between cultures. These are taken from a document of guidelines of translating and adapting tests between languages and cultures from the International Test Commission. https://www.intestcom.org/files/guideline_test_adaptation.pdf

The last chapter is entirely suggestions for future reading. The following references stood out:

[1] (Book) Educational Measurement, 4th edition, by Brennan 2006. Especially the first chapter, by Messick

[2] (Book) Hierarchical Linear Models: Applications and Data Analysis by Ravdenbush and Bryk 2002.

[3] (Book) Structural Equation Modelling with EQS by Byrne 2006. (EQS is a software package)

[4] (Book) Fundamentals of Item Response Theory, by Hambleton, Swaminthan, and Rogers 1991.

[5] (Book) Experimental and Quasi-Experimental Designs for General Causal Interance by Shadish, Cook, and Campbell 2002. (this is probably different from the ANOVA/Factorial heavy Design/Analysis of Experiments taught in undergrad stats)

[6] (Journal) New Directions in Evaluation

Sunday 29 November 2015

Tuesday 10 November 2015

I read this: Meta-Analysis, A Comparison of Approaches

My motivation for reading Meta-Analysis: A Comparison of Approaches by Ralph Schulze was to further explore the idea of a journal of replication and verification. Meta-analyses seemed like a close analogy, except that researchers are evaluating many studies together, rather than one in detail. I’m not working on any meta-analyses right now, but I may later. If you are reading this to decide if this book is right for you, consider that your motivations will differ.

Saturday 31 October 2015

A Web Crawler using R

This R-based web crawler, available here...

1. Reads the HTML of a webpage from a given address,

2. Extracts the hyperlinks from that page to other pages and files,

3. Filters out links that fail to meet given criteria (e.g. other websites, already explored, and non-html)

4. Stores the origin and destinations of the remaining links,

5. Selects a link from those discovered so far, and returns to 1.

The scraper can be used to gather raw data from thousands of pages from a website, and reveal information of the network of links between them. For example, starting just now at the front page of the National Post website, the crawler visited a news article, the main page for horoscopes, the day's horoscopes, and an article from the financial pages of the paper.

1. Reads the HTML of a webpage from a given address,

2. Extracts the hyperlinks from that page to other pages and files,

3. Filters out links that fail to meet given criteria (e.g. other websites, already explored, and non-html)

4. Stores the origin and destinations of the remaining links,

5. Selects a link from those discovered so far, and returns to 1.

The scraper can be used to gather raw data from thousands of pages from a website, and reveal information of the network of links between them. For example, starting just now at the front page of the National Post website, the crawler visited a news article, the main page for horoscopes, the day's horoscopes, and an article from the financial pages of the paper.

Wednesday 28 October 2015

Take-home lessons and code from a factor-cluster analysis with imputation

Recently I was tapped to examine data from a survey of ~200 children to find if their learning preferences fell into well-defined profiles (i.e. clusters). The relevant part of the survey had more than 50 Likert scale questions The client and I had decided that a factor analysis, followed by a cluster analysis would be most appropriate.

I learned some things in doing this analysis, and wanted to share that and some relevant code.

Sunday 18 October 2015

Teaching Philosophy Statement on Intro Math/Stats - Cartographers of Knowledge

In the digital age, a teacher's role is not simply to present knowledge, but to navigate it. The overwhelming majority of the information that an undergraduate gains in her degree is available for free on the internet or in libraries.

A digital age instructor's job is to guide and motivate students' paths through this information – to provide the vision and context necessary to develop expertise in a field. Introductory courses make up the bulk of students' collective experience with mathematics and statistics, so any expertise to be gained in those one or two courses needs to be a self-contained package.

For example, rigorous proofs serve introductory students very little; the practice of rigor and constructing proofs has little value until upper-division courses. Introductory students learn by doing the tasks that are actually relevant to the course: examples. As such, I prefer to relegate much of the proof work to optional out-of-class readings. The extra instructional time for guided, step-by-step examples makes the material more accessible. It also provides more opportunities to fill the fundamental gaps from high school mathematics that will otherwise prevent understanding. For the few that do continue in a mathematics or statistics major, I feel that what they may lack in experience with proofs is more than compensated by a stronger foundation in the introductory material.

This focus on accessibility extends to my policies on assignments and office hours. Assignments should be vehicles for students to struggle through a set of practice problems and receive formative feedback. However, logistics of providing quality feedback aside, that doesn't work for everyone. Assignments need to have grades attached so students will have extrinsic motivation to completing them, but these same grades penalize mistakes on something that should be practice.

I want assignments to be important and challenging enough to take seriously, but not so much as to tempt plagiarism. In the past, I have solved this by booking extra office hours on the days before assignments are due, and telling my students that I will give them entire solutions to assignment questions. I've found that on these office days, a group of 5-12 students would come to my office with their assignment hang-ups, but that they could answer each others' questions with only moderate guidance from me. Some of these students likely sat in to get their solutions from the rest of the office group, but that's still better than copying written assignments verbatim.

Finally, I try to explicitly declare the 'take-home messages' by including them in my lessons. That is, the few ideas that I hope students will remember long after the final exam is over. These messages include general strategies about the mathematical sciences such as “every hard problem is merely a collection of easy problems”, and George Box's quote “all models are wrong, some are useful.”. If my students are to retain anything from their time spent on coursework, I hope it's something of value and general applicability rather than memories of referring to tables of integrals and probability.

A digital age instructor's job is to guide and motivate students' paths through this information – to provide the vision and context necessary to develop expertise in a field. Introductory courses make up the bulk of students' collective experience with mathematics and statistics, so any expertise to be gained in those one or two courses needs to be a self-contained package.

For example, rigorous proofs serve introductory students very little; the practice of rigor and constructing proofs has little value until upper-division courses. Introductory students learn by doing the tasks that are actually relevant to the course: examples. As such, I prefer to relegate much of the proof work to optional out-of-class readings. The extra instructional time for guided, step-by-step examples makes the material more accessible. It also provides more opportunities to fill the fundamental gaps from high school mathematics that will otherwise prevent understanding. For the few that do continue in a mathematics or statistics major, I feel that what they may lack in experience with proofs is more than compensated by a stronger foundation in the introductory material.

This focus on accessibility extends to my policies on assignments and office hours. Assignments should be vehicles for students to struggle through a set of practice problems and receive formative feedback. However, logistics of providing quality feedback aside, that doesn't work for everyone. Assignments need to have grades attached so students will have extrinsic motivation to completing them, but these same grades penalize mistakes on something that should be practice.

I want assignments to be important and challenging enough to take seriously, but not so much as to tempt plagiarism. In the past, I have solved this by booking extra office hours on the days before assignments are due, and telling my students that I will give them entire solutions to assignment questions. I've found that on these office days, a group of 5-12 students would come to my office with their assignment hang-ups, but that they could answer each others' questions with only moderate guidance from me. Some of these students likely sat in to get their solutions from the rest of the office group, but that's still better than copying written assignments verbatim.

Finally, I try to explicitly declare the 'take-home messages' by including them in my lessons. That is, the few ideas that I hope students will remember long after the final exam is over. These messages include general strategies about the mathematical sciences such as “every hard problem is merely a collection of easy problems”, and George Box's quote “all models are wrong, some are useful.”. If my students are to retain anything from their time spent on coursework, I hope it's something of value and general applicability rather than memories of referring to tables of integrals and probability.

Monday 12 October 2015

Now you're thinking with gates!

What do Nintendo and Bitcoin enthusiasts have in common? They weren't content with solving their problems through software advancements alone. The statistical computing field shouldn't be either.

-------------------

The Super Nintendo Entertainment System is a cartridge-based system, meaning that its games were stored on circuit boards encased in plastic cartridges. Unlike disc-based media of most later generations of game consoles, the contents of cartridges were not restricted to read-only data. The most common addition to game cartridges was a small cache of re-writable memory used to store progress data in the cartridge.

Originally, active objects in games, called sprites, could only be displayed as one of a set of pre-drawn frames. That's why sprite animations are usually simple loops of a few frames, and why characters are rarely seen changing size as they move towards or away from the player's point of view.

However, later games also included special-purpose microchips that expanded the graphical capabilities of the Super Nintendo console itself. One of these chips allowed the SNES to change the way sprites look as the game was happening, which made sprites look much more alive. This chip also allowed for rudimentary three-dimensional rendering.

Any software workaround to get these effects using only the hardware given in the Super Nintendo would have taking much longer and produced much worse results, if any at all. The video on the Super Nintendo (SNES) by video game trivia group Did You Know Gaming covers these effects and the chips in more detail, and shows some great demonstrations.

------------------

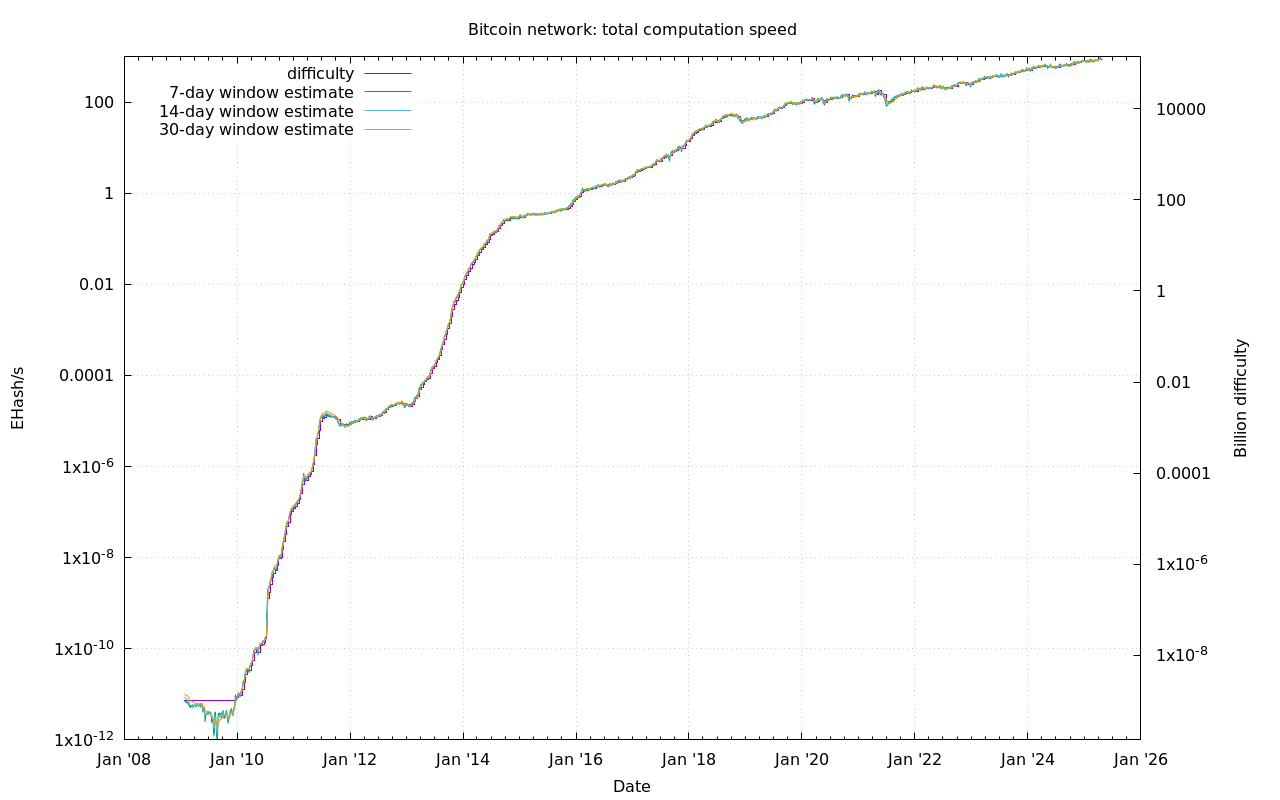

Bitcoin, is a cryptocurrency. Part of what gives it value is the premise that it is computationally hard to create or 'mine' for new ones. In fact, there is a self-adjustment mechanism that increases the mining difficulty in proportion to the total computing power of all miners.

I've appended this historical chart of the log of the total computer power (and the log difficulty), over time with the two hardware advancements that defined the trend in bitcoin mining power.

-------------------

The Super Nintendo Entertainment System is a cartridge-based system, meaning that its games were stored on circuit boards encased in plastic cartridges. Unlike disc-based media of most later generations of game consoles, the contents of cartridges were not restricted to read-only data. The most common addition to game cartridges was a small cache of re-writable memory used to store progress data in the cartridge.

Originally, active objects in games, called sprites, could only be displayed as one of a set of pre-drawn frames. That's why sprite animations are usually simple loops of a few frames, and why characters are rarely seen changing size as they move towards or away from the player's point of view.

However, later games also included special-purpose microchips that expanded the graphical capabilities of the Super Nintendo console itself. One of these chips allowed the SNES to change the way sprites look as the game was happening, which made sprites look much more alive. This chip also allowed for rudimentary three-dimensional rendering.

Any software workaround to get these effects using only the hardware given in the Super Nintendo would have taking much longer and produced much worse results, if any at all. The video on the Super Nintendo (SNES) by video game trivia group Did You Know Gaming covers these effects and the chips in more detail, and shows some great demonstrations.

------------------

Bitcoin, is a cryptocurrency. Part of what gives it value is the premise that it is computationally hard to create or 'mine' for new ones. In fact, there is a self-adjustment mechanism that increases the mining difficulty in proportion to the total computing power of all miners.

I've appended this historical chart of the log of the total computer power (and the log difficulty), over time with the two hardware advancements that defined the trend in bitcoin mining power.

{kind=link}

The first event represents the first time mining using a more specialized graphical processing unit (GPU) rather than a more general central processing unit (CPU) was made publicly possible. Since many miners had compatible graphics cards already, we see a tenfold jump in power almost instantly.

The second event represents the first time mining using a single-purpose processor, called an ASIC* was introduced to the market. This time, another rapid increase in processing power is sparked, but without the initial leap.

An ASIC is orders of magnitude faster at the simple, repetitive task of mining bitcoins than a GPU is, and a GPU mines orders of magnitude faster than a comparably priced CPU. In both cases, the new hardware quickly rendered any previous mining methods obsolete.

* Application Specific Integrated Circuit.

---------------

When developing new methods to solve computational problems, a software approach usually works best. The results of purely software-based are often portable as packaged programs, and the dissemination of improvements can be as quick and as cheap as a software update. The feedback loop of testing and improvement is very quick, and there are many languages such as the R, SAS, and Julia that can make software-based solutions a routine task.

Making hardware to solve a problem may sound insane by comparison - why would anyone willingly give up all of those advantages? This is where Field Programmable Gate Arrays come in. An FPGA is essentially a circuit board that can be programmed down to the gate level. That is, a user can write a program in terms of the fundamental particles of computation, OR, NOT, XOR, AND, and NAND gates.

The FPGA takes a set of gate instructions and physically wires itself into the programmed configuration. When set, the FPGA is essentially an ASIC, an processor that can only do one task but potentially much faster than a general purpose computer. However, if needed, an FPGA can be re-programmed, so the advantage of a quick trial-and-error turnaround is there. Also, the program can be disseminated like any other software. The most popular FPGAs cost between $200 and $500 USD.

The bitcoin ASIC started off as an FPGA. Once the FPGA program was made, it took about a year for the first ASICs to be sold. This is encouraging for anyone looking towards FPGAs for the next great leap in statistical computing, as it means the endeavor has commercial viability. Just think how much faster some common methods could become even if only large matrix inversion was made faster.

It's time to start thinking with gates.

Tuesday 8 September 2015

Arguments for Journals of Replication

In today's xkcd, a collection of hypothetical headlines are given, all of which would spell trouble for science as a whole. Also, these headlines all have to do with replicating experiments. The only fictional part of (most of) these headlines is that they're showing up in the news, because this is an old problem. Given that new journals are frequently being made as fields evolve and grow, it's surprising to not find any journals of replication and verification, because having such journals could help make science more honest.

Creating and contributing to journals dedicated to replicating, verifying, and assessing work in a field is a worthwhile endeavour. Here's why:

Primary Motivation - Having a journal of replication in a field would implicitly improve the quality of research across that field. It would do this by effectively putting a bounty on bad research by offering a publication opportunity for addressing flaws. It also provides an incentive for a team that 'gets there second' to publish, which could remove some of the unscientific competitiveness of people working towards the same goal. Finally, it provides relatively easy publication opportunities for people wishing to do the work that makes a field's body of work more cohesive by repeating key experiments or by conducting meta-studies.

Assertion 1 - Replication has high scientific value: Consider an experiment done twice, in two independent labs. It may not produce as much new information as two different experiments, but the information it does provide would be of a higher quality. That's what scientific journals are supposed to do - focus on quality. Large volumes of low quality information can be found anywhere.

Assertion 2 - Replication is easy and safe: Assuming that the method have been outlined well, someone trying to replicate an experiment can skip past a lot of the planning and false starts of the original researcher. The second research team even has the first one to ask questions. It's safe in that the chance of a new discovery, and hence publication delays, is low. This makes it suitable for the sort of mass produced work that can be outsourced to graduate students with minimal degree hiccups.

Assertion 3 - A replication journal has reward potential for contributors: Logically, most replication papers fall into two categories: Refutation or verification. If research is verified, the original researchers gain prestige and a citation, and the replicators gain a publication. In future work, many groups mentioning the original work will want to cite both papers because together they make a stronger argument. If the research if refuted, at best it could spark interest in 'tiebreaker' work by a 3rd research party, which would cite both (positively, if everything was done honestly), and at worst the original work dies early where it would or should have anyway, and the replicators establish their reputation for rigor.

Assertion 4 - A replication journal has reader appeal: If someone is reading a research paper, they may be interested how credible the work is after it has been subject to public scrutiny. A replication journal appropriate to the paper's field would be a good first place to look because it would save the reader the trouble of filtering through work that cited the paper in question or looking for otherwise related work that may lend to or take credence from the paper. In short, a replication journal would offer the same service to readers that review sites offer to consumers of more commercial goods.

Assertion 5 - A replication journal would be easy to administer: Aside from papers on related verification methods, all the relevant submissions to such a journal would be adhere to specific formulae - they would either be direct replications or metastudies. Hopefully, this would make the editing and review work of these papers easier because most viable papers would look the same: Introduction of the work to be replicated, comparison of methods, comparison of results, short discussion. Criteria for publication would have few ambiguities that require editorial decision-making.

Creating and contributing to journals dedicated to replicating, verifying, and assessing work in a field is a worthwhile endeavour. Here's why:

Primary Motivation - Having a journal of replication in a field would implicitly improve the quality of research across that field. It would do this by effectively putting a bounty on bad research by offering a publication opportunity for addressing flaws. It also provides an incentive for a team that 'gets there second' to publish, which could remove some of the unscientific competitiveness of people working towards the same goal. Finally, it provides relatively easy publication opportunities for people wishing to do the work that makes a field's body of work more cohesive by repeating key experiments or by conducting meta-studies.

Assertion 1 - Replication has high scientific value: Consider an experiment done twice, in two independent labs. It may not produce as much new information as two different experiments, but the information it does provide would be of a higher quality. That's what scientific journals are supposed to do - focus on quality. Large volumes of low quality information can be found anywhere.

Assertion 2 - Replication is easy and safe: Assuming that the method have been outlined well, someone trying to replicate an experiment can skip past a lot of the planning and false starts of the original researcher. The second research team even has the first one to ask questions. It's safe in that the chance of a new discovery, and hence publication delays, is low. This makes it suitable for the sort of mass produced work that can be outsourced to graduate students with minimal degree hiccups.

Assertion 3 - A replication journal has reward potential for contributors: Logically, most replication papers fall into two categories: Refutation or verification. If research is verified, the original researchers gain prestige and a citation, and the replicators gain a publication. In future work, many groups mentioning the original work will want to cite both papers because together they make a stronger argument. If the research if refuted, at best it could spark interest in 'tiebreaker' work by a 3rd research party, which would cite both (positively, if everything was done honestly), and at worst the original work dies early where it would or should have anyway, and the replicators establish their reputation for rigor.

Assertion 4 - A replication journal has reader appeal: If someone is reading a research paper, they may be interested how credible the work is after it has been subject to public scrutiny. A replication journal appropriate to the paper's field would be a good first place to look because it would save the reader the trouble of filtering through work that cited the paper in question or looking for otherwise related work that may lend to or take credence from the paper. In short, a replication journal would offer the same service to readers that review sites offer to consumers of more commercial goods.

Assertion 5 - A replication journal would be easy to administer: Aside from papers on related verification methods, all the relevant submissions to such a journal would be adhere to specific formulae - they would either be direct replications or metastudies. Hopefully, this would make the editing and review work of these papers easier because most viable papers would look the same: Introduction of the work to be replicated, comparison of methods, comparison of results, short discussion. Criteria for publication would have few ambiguities that require editorial decision-making.

Tuesday 4 August 2015

Lesson Prototype - First Lecture on Multiple Imputation

Continuing the work on my data management course, here's the start of the Imputation unit. I'm intending three units in total - Text processing, principles of data manipulation (cleaning, merging, formatting, and database access), and imputation.

Friday 31 July 2015

Possible Application of Approximate Bayesian Computation for Networks

I've been thinking about possible applications for the network simulation/analysis program that Steve Thompson and I developed as part of my PhD thesis.*

I propose to investigate the effect of response order/timing in respondent-driven sampling on estimates of network parameters.

Here I'm assuming that samples are taken in waves. That is, a collection of seed members of the population are identified and given the initial coupons. If the standard deviation of the response times is small compared to the mean, the network of the population is being sampled in a manner similar to breadth first search (BFS). If the standard deviation of response times is large relative the mean, the network ends up being sampled in a manner closer to that of a depth first search (DFS). Each of these sampling methods has the potential to provide vastly different information about the sample.

Such an investigation would include four parts:

1) Motivating questions: Why would we care about the time it takes members of the population to be entered into the sample? Because perhaps these times could be influenced by different incentive structures. If they can, what is best? If they cannot, we can do a what-if analysis to explore counter-factuals. Does timing matter? What sampling and incentive setups are robust to the effects of response times? Are there statistical methods that can adjust for the effects of response times?

2) Find some real respondent-driven samples, preferably by looking in the literature of PLoS-One and using the data that is included with publications, but possibly by asking other researchers individually.

Look at the time stamp of each observation in each data set, if available, and fit a distribution such as gamma(r, beta) to the time delay between giving a recruitment coupon and that recruitment coupon being used. Compare the parameter estimates that each data set produces to see if there is a significant difference between them and see if there's any obvious reason or pattern behind the changes.

3) Generate a few networked populations and sample from each one many times using the different response-delay time distributions found in Part 2. Are there any significant changes to the network statistics that we can compute from the samples we find? That is, how does the variation of the statistics between resamples under one delay time distribution compare to the variation between delay time distributions?

4) Employ the full ABCN system to get estimates of whatever network parameters we can get for case ij, 1 <= i,j <= M, where M is the number of datasets we find. Case ij would be using the observed sample from the ith dataset, with simulations in the ABCN system using the delay distribution estimated from the jth dataset.

This way, we could compare the variation in the network parameters attributable to the sample that was actually found, and how much was attributable to the difference in time it took for recruitments to be entered into the survey. Also, we effectively will have performed a what-if analysis on the datasets we use - and seeing if the conclusions from the datasets would have been different if the recruited respondents had been responded with different delay structures.

---------------------------------------

*This network simulation/analysis system takes an observed sample of network and computes a battery of summarizing statistics of the sample. Then it simulates and samples from many networks and computes the same battery from each sample. It estimates the parameters of the original sample by looking at the distribution of parameters from the simulation samples that were found to be similar to the observed sample.

This will all be explained again, and in greater detail when I post my thesis after the defense in... gosh.. a month. Basically it's statistical inference turned upside down, where you generate the parameters and see if they make the sample you want, instead of starting with the sample and estimating a parameter value or distribution. The base method is called Approximate Bayesian Computation.

I propose to investigate the effect of response order/timing in respondent-driven sampling on estimates of network parameters.

Here I'm assuming that samples are taken in waves. That is, a collection of seed members of the population are identified and given the initial coupons. If the standard deviation of the response times is small compared to the mean, the network of the population is being sampled in a manner similar to breadth first search (BFS). If the standard deviation of response times is large relative the mean, the network ends up being sampled in a manner closer to that of a depth first search (DFS). Each of these sampling methods has the potential to provide vastly different information about the sample.

Such an investigation would include four parts:

1) Motivating questions: Why would we care about the time it takes members of the population to be entered into the sample? Because perhaps these times could be influenced by different incentive structures. If they can, what is best? If they cannot, we can do a what-if analysis to explore counter-factuals. Does timing matter? What sampling and incentive setups are robust to the effects of response times? Are there statistical methods that can adjust for the effects of response times?

2) Find some real respondent-driven samples, preferably by looking in the literature of PLoS-One and using the data that is included with publications, but possibly by asking other researchers individually.

Look at the time stamp of each observation in each data set, if available, and fit a distribution such as gamma(r, beta) to the time delay between giving a recruitment coupon and that recruitment coupon being used. Compare the parameter estimates that each data set produces to see if there is a significant difference between them and see if there's any obvious reason or pattern behind the changes.

3) Generate a few networked populations and sample from each one many times using the different response-delay time distributions found in Part 2. Are there any significant changes to the network statistics that we can compute from the samples we find? That is, how does the variation of the statistics between resamples under one delay time distribution compare to the variation between delay time distributions?

4) Employ the full ABCN system to get estimates of whatever network parameters we can get for case ij, 1 <= i,j <= M, where M is the number of datasets we find. Case ij would be using the observed sample from the ith dataset, with simulations in the ABCN system using the delay distribution estimated from the jth dataset.

This way, we could compare the variation in the network parameters attributable to the sample that was actually found, and how much was attributable to the difference in time it took for recruitments to be entered into the survey. Also, we effectively will have performed a what-if analysis on the datasets we use - and seeing if the conclusions from the datasets would have been different if the recruited respondents had been responded with different delay structures.

---------------------------------------

*This network simulation/analysis system takes an observed sample of network and computes a battery of summarizing statistics of the sample. Then it simulates and samples from many networks and computes the same battery from each sample. It estimates the parameters of the original sample by looking at the distribution of parameters from the simulation samples that were found to be similar to the observed sample.

This will all be explained again, and in greater detail when I post my thesis after the defense in... gosh.. a month. Basically it's statistical inference turned upside down, where you generate the parameters and see if they make the sample you want, instead of starting with the sample and estimating a parameter value or distribution. The base method is called Approximate Bayesian Computation.

Sunday 26 July 2015

Prediction Assisted Streaming

The online game path of exile has a trick for reconciling a game that requires quick reaction times with the limitations of servers: it predicts the actions of the players. It doesn't have to predict far ahead - a couple hundred milliseconds - to keep the action running smoothly most of the time.

Prediction on this time frame isn't hard in principle; play often involves performing the same short

action repeatedly, such as firing an arrow, so the default prediction is just more of that. When the server predicts incorrectly, it usually has enough time to 'rewind' to the present and handle things as they come. The prediction is just an extra buffering layer that's in place when there is a lot of server lag.

Does video or music streaming do this? Could it?

In a song with a repetitive baseline, could the information to the client computer include: "repeat the sound from time x with the following deviations included in the buffer", rather than "play the following sound"? The "sound at time x" in this case is a note from the baseline and the deviations being the result of a human playing an instrument and not hitting the note exactly the same every time. In a case like that, potentially less data would need to be sent to reproduce the song, allowing for longer buffers or higher sound quality.

Likewise for video. Consider a live video feed of a soccer match, in which a player is running across the field. Video prediction may determine there is an object moving at some speed in some direction and predict a few frames ahead where that object will be, and thus what pixels to draw in that spot. Then the streaming service, making the same prediction, could just send the video information that deviates from this prediction.

For repetitive patterns like an animation of a like a spinning wheel or sparkling logo of a sports team. If the wheel spins in a predictable fashion, internet bandwidth could be saved by describing the movement of the wheel as "spinning as expected", where matching prediction software on the server and client sides both recognize that that part of the screen is taken up by an object in 10-frame loop.

This is different from encoding only the pixels that change from frame to frame. This prediction would incorporate likely changes in a picture based on simple movement patterns or on repetitive animations.

Consider a streaming game of hearthstone, like the last time I pretended to know about video encoding. There are certain animations that regularly impact video quality, such as sand sweeping across the entire screen, that involve a many pixels changing for a non-trivial amount of time. The video encoder does fine when the picture is mostly the same from frame to frame, but introduce one of these effects that causes a lot of pixels change at once, and the quality of the live stream.

{kind=link}

However, the sand effect is one of sand moving slowly across the screen, its movement is predictable in that any one pixel of the effect is likely to follow the same trajectory as it did in the last few frames. Predictive video encoding is more scalable than the application specific encoding I mentioned before, but with time it could achieve the same effect if it was able to recognize frequently used pre-rendered effects such as lightning all over the screen. A predictive video encoder could recognize the first few frames of the 'lightning storm' effect and predict the rest without having to send any information about that part of the screen.

{kind=link}

I'm no expert on video encoding, so this may all be jibberish.

Previous post on video encoding in Twitch, the possibility of application specific codecs.

Sunday 19 July 2015

Using optim() to get 'quick and dirty' solutions, a case study on network graphs

The optim() function in base R, is a generalized optimizer for continuous functions. It looks for the minimum of some objective function that you define across some continuous parameter space that you define.

In this post, I show how to use optim() to find a (inelegant, but workable) solution to do something very complex, plot a network of nodes based on the shortest path between them, with relatively little programming effort.

In this post, I show how to use optim() to find a (inelegant, but workable) solution to do something very complex, plot a network of nodes based on the shortest path between them, with relatively little programming effort.

Saturday 11 July 2015

Danni and Jeremy's Wedding Speech

As requested, here is the speech that was given for Danni-Lynn Laidlaw and Jeremy Strang's wedding last month.

[Party 1] was Danni-Lynn

[Party 2] was Jeremy

[Member of Audience] was Calen, Danni's brother.

Regular text represents my own additions

Italic text is taken verbatim from the Government of British Columbia's standard ceremony,

of which the bold italic parts are immutable and cannot be changed.

Anything in underline is spoken by one of the two parties being married.

The standard ceremony can be found at http://www2.gov.bc.ca/assets/gov/residents/vital-statistics/marriages/vsa718.pdf

-----------------------------------------------

Majestic Ladies, Handsome Gentlemen, and [Member of Audience].

We have assembled here to acknowledge a force that ruthlessly devoured billions before and will no doubt continue to consume live in their prime until the sky crumbles.

This remorseless and unceasing force is called love. These two, though their forms appear before you, are hopelessly lost -- beyond mourning , really.

Today we witness the passing of [Party 1] and [Party 2] into the penultumate stage of their falling to this force. The true word for this stage makes all who hear it cry blood and vomit leeches. Thankfully I lack the four tongues required to pronounce it. However, even the English word has terrified lesser men before. That word is "marriage".

The state of matrimony, as understood by us, is a state ennobled and enriched by a long and honourable tradition of devotion, set in the basis of the law of the land, assuring each participant an equality before the law, and supporting the common right of each party to the marriage.

There is assumed to be a desire for life-long companionship, and a generous sharing of the help and comfort that a couple ought to have from each other, through whatever circimstances of sickness or health, joy or sorrow, proserity or adversity, the lives of these parties may experience.

Marriage is therefore not to be entered upon thoughtlessly or irresponsibly, but with a due and serious understanding and appreciation of the ends for which it is undertaken, and of the material, intellectual, and emotional factors which will govern its fullfillment.

It is by its nature a state of giving rather than taking, of offering rather than receiving, for marriage requires the giving of one's self to support the marriage and the marriage and the home in which it may flourish.

It is into this high and serious state that these two persons desire to unite.

Therefore:

I charge and require of you both in the presence of these witnesses, that if either of you know of any legal impediment to this marriage, you do now reveal the same.

Let [Party 1] repeat after me:

"I solemnly declare that I do not know of any lawful impediment why I, [Person 1] may not be joined in matrimony to [Person 2]."

Let [Party 2] repeat after me:

"I solemnly declare that I do not know of any lawful impediment why I, [Person 2] may not be joined in matrimony to [Person 1]."

There having been no reason given why this couple may not be married, nor any reasonless jibbering that could be interpreted as such, I ask you to give answer to these questions.

Do you [Party 1] undertake to afford to [Party 2] the love of your person, the comfort of your companionship,m and the patience of your understanding, to respect the dignity of their person, their own inalienable personal rights, and to recognize the right of counsel and the consultation upon all matters relating to the present, future, and alternate realities of the household established by this marriage?

(A prompt of 'do you, or do you not' may help here)

[Party 1]: I do.

Do you [Party 2] undertake to afford to [Party 1] the love of your person, the comfort of your companionship,m and the patience of your understanding, to respect the dignity of their person, their own inalienable personal rights, and to recognize the right of counsel and the consultation upon all matters relating to the present, future, and alternate realities of the household established by this marriage?

(Again, a prompt of 'do you, or do you not' may help here. Especially because doing it twice makes it sound planned)

[Party 2]: I do.

Let the couple join their right hands, claws, tentacles, feelers, probosci, or pseudopods, and let [Party 1] repeat after me.

I call on those present to witness that I, [Party 1], take [Party 2] to be my lawful wedded (wife/husband/spouse), to have and hold, from this day forward, in madness and in health, in whatever circumstances life may hold for us.

and let [Party 1] repeat after me.

I call on those present to witness that I, [Party 1], take [Party 2] to be my lawful wedded (wife/husband/spouse), to have and hold, from this day forward, in madness and in health, in whatever circumstances life may hold for us.

Inasmuch as you have made this declaration of your vows concerning one another, and have set these rings before me, I ask that now these rings be used and regarded as a seal and a confirmation and acceptance of the vows you have made.

Let [Party 1] place the ring on the third noodly appendage of [Party 2]'s left hand, repeat after me:

With this ring, as the token and pledge of the vow and covenant of my word, I call upon those persons present, and those unpersons lurking among us beyond mortal sight, that I, [Party 1], do take thee [Party 2], to be my lawful wedded (wife/husband/spouse)

Let [Party 2] say after me:

In receiving this ring, being the token and pledge of the covenant of your word, I call upon those persons present to witness that I [Party 2] do take thee [Party 1] to be my lawful wedded (wife/husband/spouse).

Let [Party 2] place the ring on the third noodly appendage of [Party 1]'s left hand, repeat after me:

With this ring, as the token and pledge of the vow and covenant of my word, I call upon those persons present, and those unpersons lurking among us beyond mortal sight, that I, [Party 2], do take thee [Party 1], to be my lawful wedded (wife/husband/spouse)

Let [Party 1] say after me:

In receiving this ring, being the token and pledge of the covenant of your word, I call upon those persons present to witness that I [Party 1] do take thee [Party 2] to be my lawful wedded (wife/husband/spouse).

And now, forasmuch as you [Party 1] and [Party 2] have consented to legal wedlock, and have declared your solemn intention in this company, before these witnesses, and in my presence, and have exchanged these rings as the pledge of your vows to each other, now upon the authority vested in me by the province of British Columbia, I pronounce you as duly married.

You may kiss.

[Party 1] was Danni-Lynn

[Party 2] was Jeremy

[Member of Audience] was Calen, Danni's brother.

Regular text represents my own additions

Italic text is taken verbatim from the Government of British Columbia's standard ceremony,

of which the bold italic parts are immutable and cannot be changed.

Anything in underline is spoken by one of the two parties being married.

The standard ceremony can be found at http://www2.gov.bc.ca/assets/gov/residents/vital-statistics/marriages/vsa718.pdf

-----------------------------------------------

Majestic Ladies, Handsome Gentlemen, and [Member of Audience].

We have assembled here to acknowledge a force that ruthlessly devoured billions before and will no doubt continue to consume live in their prime until the sky crumbles.

This remorseless and unceasing force is called love. These two, though their forms appear before you, are hopelessly lost -- beyond mourning , really.

Today we witness the passing of [Party 1] and [Party 2] into the penultumate stage of their falling to this force. The true word for this stage makes all who hear it cry blood and vomit leeches. Thankfully I lack the four tongues required to pronounce it. However, even the English word has terrified lesser men before. That word is "marriage".

The state of matrimony, as understood by us, is a state ennobled and enriched by a long and honourable tradition of devotion, set in the basis of the law of the land, assuring each participant an equality before the law, and supporting the common right of each party to the marriage.

There is assumed to be a desire for life-long companionship, and a generous sharing of the help and comfort that a couple ought to have from each other, through whatever circimstances of sickness or health, joy or sorrow, proserity or adversity, the lives of these parties may experience.

Marriage is therefore not to be entered upon thoughtlessly or irresponsibly, but with a due and serious understanding and appreciation of the ends for which it is undertaken, and of the material, intellectual, and emotional factors which will govern its fullfillment.

It is by its nature a state of giving rather than taking, of offering rather than receiving, for marriage requires the giving of one's self to support the marriage and the marriage and the home in which it may flourish.

It is into this high and serious state that these two persons desire to unite.

Therefore:

I charge and require of you both in the presence of these witnesses, that if either of you know of any legal impediment to this marriage, you do now reveal the same.

Let [Party 1] repeat after me:

"I solemnly declare that I do not know of any lawful impediment why I, [Person 1] may not be joined in matrimony to [Person 2]."

Let [Party 2] repeat after me:

"I solemnly declare that I do not know of any lawful impediment why I, [Person 2] may not be joined in matrimony to [Person 1]."

There having been no reason given why this couple may not be married, nor any reasonless jibbering that could be interpreted as such, I ask you to give answer to these questions.

Do you [Party 1] undertake to afford to [Party 2] the love of your person, the comfort of your companionship,m and the patience of your understanding, to respect the dignity of their person, their own inalienable personal rights, and to recognize the right of counsel and the consultation upon all matters relating to the present, future, and alternate realities of the household established by this marriage?

(A prompt of 'do you, or do you not' may help here)

[Party 1]: I do.

Do you [Party 2] undertake to afford to [Party 1] the love of your person, the comfort of your companionship,m and the patience of your understanding, to respect the dignity of their person, their own inalienable personal rights, and to recognize the right of counsel and the consultation upon all matters relating to the present, future, and alternate realities of the household established by this marriage?

(Again, a prompt of 'do you, or do you not' may help here. Especially because doing it twice makes it sound planned)

[Party 2]: I do.

Let the couple join their right hands, claws, tentacles, feelers, probosci, or pseudopods, and let [Party 1] repeat after me.

I call on those present to witness that I, [Party 1], take [Party 2] to be my lawful wedded (wife/husband/spouse), to have and hold, from this day forward, in madness and in health, in whatever circumstances life may hold for us.

and let [Party 1] repeat after me.

I call on those present to witness that I, [Party 1], take [Party 2] to be my lawful wedded (wife/husband/spouse), to have and hold, from this day forward, in madness and in health, in whatever circumstances life may hold for us.

Inasmuch as you have made this declaration of your vows concerning one another, and have set these rings before me, I ask that now these rings be used and regarded as a seal and a confirmation and acceptance of the vows you have made.

Let [Party 1] place the ring on the third noodly appendage of [Party 2]'s left hand, repeat after me:

With this ring, as the token and pledge of the vow and covenant of my word, I call upon those persons present, and those unpersons lurking among us beyond mortal sight, that I, [Party 1], do take thee [Party 2], to be my lawful wedded (wife/husband/spouse)

Let [Party 2] say after me:

In receiving this ring, being the token and pledge of the covenant of your word, I call upon those persons present to witness that I [Party 2] do take thee [Party 1] to be my lawful wedded (wife/husband/spouse).

Let [Party 2] place the ring on the third noodly appendage of [Party 1]'s left hand, repeat after me:

With this ring, as the token and pledge of the vow and covenant of my word, I call upon those persons present, and those unpersons lurking among us beyond mortal sight, that I, [Party 2], do take thee [Party 1], to be my lawful wedded (wife/husband/spouse)

Let [Party 1] say after me:

In receiving this ring, being the token and pledge of the covenant of your word, I call upon those persons present to witness that I [Party 1] do take thee [Party 2] to be my lawful wedded (wife/husband/spouse).

And now, forasmuch as you [Party 1] and [Party 2] have consented to legal wedlock, and have declared your solemn intention in this company, before these witnesses, and in my presence, and have exchanged these rings as the pledge of your vows to each other, now upon the authority vested in me by the province of British Columbia, I pronounce you as duly married.

You may kiss.

Sunday 31 May 2015

First thoughts on narrative reporting

I just finished reading The Mayor of Aihara, a biography of a man named Aizawa from rural Japan derived from 1885-1925 of his daily journal. It was the first history book I've read in six years.

I read it because I wanted to get a sense of how non-fiction is written outside of the sciences. The content was good, but it was the style I was looking for, which turned out to be a 160 pages of narrative sandwiched between two 20-page blocks of analysis and commentary.

The introductory chapter discusses the limitations of the biography as a view into the life of the Japanese as a whole. It also gives some general context of the world that Aizawa lived in.

The next five chapters cover blocks of Aizawa's life. Events within each chapter are told mostly in chronological order. There is some jumping around to help organize the material into something like story arcs, except that it's almost all about one person.

In other places, details that the biography author couldn't possibly have known are included, such as the details of Aizawa's birth, and the reasoning behind the local police officer having a bicycle.

Sometimes the author's interpretations are injected, such as that Aizawa was mostly unaware of the plight of the tenant farmers in his village, and that he cared more about his family than was typical. (In the conclusion chapter, some of these assumptions are justified.)

These aspects gave the biography more cohesion as a story, with clearer connections between cause and effect, than Aizawa's life likely had in reality. I didn't mind much because it made the material easier to read, track, and remember.

Still, the reporting is subjective, not just where necessary, but also where the author could improve the work's narrative quality without sacrificing much accuracy. Contrast that to scientific reporting : when doing a chemistry experiment properly, every scientist should produce identical lab notes and the resultant reports should provide the same information regardless of who produced them. If someone else were to examine Aizawa's journal, even if they had the same background in Japanese history as the biography author, they would produce a biography with different information.

This focus on narrative in providing facts is perplexing but the rationale is visible.

Friday 8 May 2015

The end of jobs

A friend recently asked me if I foresee any chance of "jobs", or in his words "the economic trade of labour in return for payment" becoming so unsustainable that we as society would abandon it. My response is below.

-----------------

No.

The term "chance" implies that I'm not certain about the unsustainability.

There will NEVER be enough meaningful jobs for everyone. Unemployment is only in a 'healthy' range around 6-7% right now because of a system stretched to its utter limit to create jobs, often at the cost of getting meaningful work done.

First, self employment is counted as jobs in this statistic, as is part time work. So the proportion of people that trade their labour for payment likely a lot smaller than official surface figures.

There are also a large portion of jobs that simply shouldn't be.

- Literally pointless jobs like full-service gas pumps. Really gas stations could be fully automated and could behave like large vending machines.

- Parasitic jobs such as car salespeople, day traders and arbitrageurs. I separate these from pointless jobs because they do perform a service, but only because of legacy systems that mandate that these services are necessary.

- Fields where the output of the field is only loosely related to the number of people working in the field, such as marketing. From the perspective of companies, if half of all ads disappears, the only real effect would be for each remaining ad to be twice as effective. Likewise, the benefit to the consumer, knowledge of a product, would be just as large with perhaps only 10% of ads retained. In that sense, 90% of the work in advertising, from ad creation to posting billboards, is parasitic.

Then there are the jobs that won't be for much longer.

- Physical jobs that are due for automation, such as semi-truck driving.

- Small manufacturing jobs that can be simply replaced by on-demand 3D printing.

- Technical jobs that routinely get automated, like how much search engines have supplanted librarians.

- Many service jobs are a fixed portion of the population, such as teaching, haircutting, and child care. However, the population of countries in the developed world are either flat, declining, or dependant upon immigration to maintain the population increase that modern economics relies upon so dearly.

- Many resource-based jobs are at risk to better energy efficiency, better labour efficiency, and automated landfill harvesting and reclaimation. Even argiculture is being turned upside down by cultured meat. With it, there goes shipping.

Finally, the work that NEEDS to be done such as environmental restoration, medical services, and the development of space technology, simply doesn't work well under an exchange-for-payment system because economically 'rational' people and corporations either won't or can't pay for it.

I would refer you to the 20 minute video "Humans Need Not Apply" for a compelling argument about how this is inevitable. My best resources for universal basic income and on post-scarcity are the novels Accelerando and Red Mars touch on these topics.

-----------------

No.

The term "chance" implies that I'm not certain about the unsustainability.

There will NEVER be enough meaningful jobs for everyone. Unemployment is only in a 'healthy' range around 6-7% right now because of a system stretched to its utter limit to create jobs, often at the cost of getting meaningful work done.

First, self employment is counted as jobs in this statistic, as is part time work. So the proportion of people that trade their labour for payment likely a lot smaller than official surface figures.

There are also a large portion of jobs that simply shouldn't be.

- Literally pointless jobs like full-service gas pumps. Really gas stations could be fully automated and could behave like large vending machines.

- Parasitic jobs such as car salespeople, day traders and arbitrageurs. I separate these from pointless jobs because they do perform a service, but only because of legacy systems that mandate that these services are necessary.

- Fields where the output of the field is only loosely related to the number of people working in the field, such as marketing. From the perspective of companies, if half of all ads disappears, the only real effect would be for each remaining ad to be twice as effective. Likewise, the benefit to the consumer, knowledge of a product, would be just as large with perhaps only 10% of ads retained. In that sense, 90% of the work in advertising, from ad creation to posting billboards, is parasitic.

Then there are the jobs that won't be for much longer.

- Physical jobs that are due for automation, such as semi-truck driving.

- Small manufacturing jobs that can be simply replaced by on-demand 3D printing.

- Technical jobs that routinely get automated, like how much search engines have supplanted librarians.

- Many service jobs are a fixed portion of the population, such as teaching, haircutting, and child care. However, the population of countries in the developed world are either flat, declining, or dependant upon immigration to maintain the population increase that modern economics relies upon so dearly.

- Many resource-based jobs are at risk to better energy efficiency, better labour efficiency, and automated landfill harvesting and reclaimation. Even argiculture is being turned upside down by cultured meat. With it, there goes shipping.

Finally, the work that NEEDS to be done such as environmental restoration, medical services, and the development of space technology, simply doesn't work well under an exchange-for-payment system because economically 'rational' people and corporations either won't or can't pay for it.

I would refer you to the 20 minute video "Humans Need Not Apply" for a compelling argument about how this is inevitable. My best resources for universal basic income and on post-scarcity are the novels Accelerando and Red Mars touch on these topics.

Wednesday 6 May 2015

Prelude to a FUSS

I apologize in advance if this one is incoherent, as most of it has come in fever dreams over the last couple days.

I want to make a FUSS. That is, a Formula-Unspecified System Solver.

Saturday 18 April 2015

Using Sampling Order in Network Inference

In this previous post, I had talked about how the order of values were sampled, but I gave a pretty esoteric argument involving compression and loss of information in a sample of 8 values.

For my current thesis project, I'm developing an inference methodology for snowball samples. Snowball samples, or more generally respondent driven samples, are used to sample hard-to-reach populations or to explore network structure. The sampling protocol I'm working with is

For my current thesis project, I'm developing an inference methodology for snowball samples. Snowball samples, or more generally respondent driven samples, are used to sample hard-to-reach populations or to explore network structure. The sampling protocol I'm working with is

- Select someone to interview from the population by simple random sampling.

- In the interview, ask that person the number of connections they have (where the definition of a 'connection' is defined by the study; it could be business partners, sexual partners, close friends, or fellow injection drug users.)

- For each connection the interviewed person has, give that person a recruitment coupon to invite that connected person to come in for an interview, often with an incentive.

- If no connected person responds, go to Step 1 and repeat.

- If one connected person responds, go to Step 2 and repeat.

- If multiple people respond, go to Step 2 and interview each of them.

In reality, people are interviewed in the order they come in for an interview. In my simulation, people are interviewed in a breadth first search system, in which I assume connections to the first interviewed person are followed before any connections to those connections are followed. This may make a difference (which I will explore later), because of two limitations of the sample this protocol is modeled after:

- When the desired sample size has been attained, no more people are interviewed, even if additional people respond to the invitation. (Budget limitation)

- Connections that lead back to people already in the sample are ignored. Even the information about there being a connection is missing. (Confidentiality limitation)

The budget limitation implies that the interviewing order impacts the subjects that are included in the sample, which in turn affects any statistics measured, even those for which sampling order is ancillary.

The limitation on reported connections implies that the observed network structure is dependent upon the sampling order, even when controlling for the actual members of a sample. For example, if someone receives invitation coupons from multiple connections, they will only show up as directly connected to the first person whose coupon they use. The other connections may not even be observed to be the same network component, even though they must be by definition.

Furthermore, every sampled network will be a forest. That is, a collection of one or more trees - networks that have no cycles, connections 'back into themselves'. Only being able to observe these tree sub-networks of the actual network limits what inferences can be made about the network as a whole. Observed link density isn't very useful for well-connected graphs because the observed link density is maximal just shy of one link/node, in cases where the observed network is one huge component.

Alternate measures of density, like component diversity, ( the Shannon species diversity index, applied to the components that nodes are in), run into this problem as well. In Figure 1 below, component diversity is useless at estimating the average (responding) degree of the network for networks with more than 1.5 links/node.

|

| Figure 1, a network measure based only on observed network structure. |

However, we can also estimate things like dPr(used)/dt, the rate of change in the proportion of a sample's connections that are also included in the sample over time. Barring variation due to response rate, we would consider such a measure to be non-positive.

For networks that are sparse in large populations, the rate of change should be near zero, because very few connections will lead back into nodes that were already explored. What few recruitments there are will be just as successful up until near the end of the sample when a few may be turned away.

However, for well-connected networks, sampling is done much more often by recruitment rather than by simple random sample. As more a component network is explored, the chance that each successive connection followed leading to someone already in the sample increases. Therefore, for well connected graphs, we would expect dPr(used)/dt to be distinctly negative.

As Figure 2 shows below, we can use the rate of change in successes to differentiate between populations up to 2.5 links/node, even though most of the networks that we observe from 1.5-2.5 links/node all show up as single large components. Also note how poorly dPr(used)/dt differentiates between networks in the region where the structure-based diversity index excels.

|

| Figure 2, a network measure based on sampling order. |

Measures like these, in combination, can be used to make estimates of the features of the population as a whole, but that's for a poster I'm working in the coming weeks.

Monday 13 April 2015

Temporary Blogging Slowdown, Future Plans

It was my original intention to publish four posts on this blog throughout each week. However, I am currently in the last few months of my PhD thesis in Statistics at Simon Fraser University.

Most of my writing effort is being funneled into that in the hopes of defending before the end of next semester. As such, any posts that appear here until the thesis is submitted will be less frequent and of lower effort, such as the laser tag ranking post instead of the goal difference average posts.

With luck, there will be a burst of high-quality material here in here in the late summer and fall to make up for the slack and bring the average back to 4+ good posts per month. I have a lot left to write about, including:

- Snowball sampling and the network analysis work I'm doing currently.

- Milaap, Kiva, Sunfunder, and lending for good and profit.

- Driving forces behind application specific integrated integrated circuits (ASICs), specifically Bitcoin and Super Nintendo.

- FPGAs , and a pipe dream to build an ASIC for large matrix operations.

- Dealing with scrap textiles, composting, crafting, and future industrial needs.

- Some arguments for landfills being the future of mining. Methane harvests, leachate harvests, necessary drilling advances, and the possible gamification of sorting trash.

- Mental health in academia, and mental health personally.

- Many more kudzu levels.

- Plans for a kudzu app, and a pipe dream of making it a carbon negative game through ad revenue and the European Carbon Exchange.

- An essay on how we all suffer from diversity defecits in heavily gendered fields, as written by a white, Anglophone, heterosexual, cis, middle class man from a nuclear family in the suburbs. (Not a satire, despite the title)

- ongoing development of a senior undergrad course on data formatting and management,

- more R package spotlights, with priority on mice for multiple imputation, and on gologit for modelling ordinal data.

- ongoing development of the R packette for sums of variables.

- ongoing development of an R packette on "debinning", and the methodology surrounding the partial recovery of within-bin data from binned data and covariate information.

- A 'to do' list for humanity, and preparation for a world of automation.

- A commentary on the energy transistion, peak child, and how the tar sands, arctic drilling, and shale fields cannot possibly be profitable in the long term.

Sunday 29 March 2015

Laser Tag Rating System

This is a rough outline of an idea that Phil Ophus and I had. We want a rating system for laser tag. We want it to be a cumulative reflection of a player's skill over multiple games. We want a means to compare the laser tag skill of players that have a substantial play record, but not necessarily against each other in the same match. In short, we want an Elo or Trueskill style metric that is a shorthand for "this player is X skilled at laser tag".

However, laser tag has less standardization than the sports and games that these metrics are usually applied to.

As it is now, the single game score cards don't give any context of a skill outside of the single match displayed. Scores in general are higher in matches with many players and longer 'ironman' matches. A score of 50000 can demonstrate just as much achievement as a score of 100000 against equally skilled opponents by these factors alone.

There are strategy factors that affect score that don't fairly reflect skill such as picking mostly weak targets, and aggressive running around play rather than base protection. Besides within-game luck, other random noise is added in from equipment effects; some guns are in better shape than others.

Scores are naturally different between free for all and team games, and some players do better in different formats. However, it's reasonable to assume a strong enough association between the skill levels of a given player across formats that one format can inform the other.

All of this variation, and this is only from a single location: Planet Lazer near Braid Station, New Westminster. At this location, the scoring system rewards hitting much more than it penalizes being hit. Also, every target on a vest is worth the same amount, although this isn't necessarily true at other locations.

We want a ratings method that can be used to compare players in different arenas that may be using different rules. Ideally something anyone could see how well they stack up on a regional up to a worldwide level. However even if we only use places that use comparable equipment, the arenas are substantially different, whereas in many other sports the arena effect is negligible. The rules and scoring systems even differ from place to place.

Our intuition and short train ride's worth of literature searching suggest that no such system exists yet that can handle the non uniform, free for all situations of laser tag. I'm hoping that further developing the cricket similalulator to handle data of cricket players that are compete in multiple formats for multiple teams in a single year.

On the sampling design and logistics side, there are issues with data collection. What if a location's equipment doesn't record a key variable? How long is data retained? Are there enough return players? It seems like the next step is to draw up a research proposal, and bring it to planet Lazer and see if they would let us record their player data like that.

For after the thesis, if at all.

Sunday 15 March 2015

R Packette - Weighted Binomial Sums

This R code file Weighted_BinSum.r is a... packette? Proto-package? Mini-package?

It's by no means a full R package because it doesn't have the proper documentation, but it's the start of what could be one.

It's by no means a full R package because it doesn't have the proper documentation, but it's the start of what could be one.

Tuesday 10 March 2015

Improving the Exam Experience - A Research Proposal

I've read through quite a few reports on improvements in university learning in the last year. A few ideas have made quite an impression. Ideas like the flipped classroom paradigm, in which the lecture time is spent working through homework problems with the guidance of the instructor and peers, and instruction and note-taking happens before the class with the use of online videos.

However, I've only seen a few pieces on improving the exam experience. Students spend a lot of time thinking about their exam performance, but besides writing good questions (which is a difficult art in itself), not much thought on the instructor side seems to have gone into it.

However, I've only seen a few pieces on improving the exam experience. Students spend a lot of time thinking about their exam performance, but besides writing good questions (which is a difficult art in itself), not much thought on the instructor side seems to have gone into it.

Sunday 8 March 2015

Kuzdu Update - Lock and Key

New Material:

First, there is a new dungeon available: Lock and Key, which features a pair of new spaces. Most of the map is sparse for treasure except for an optional room in the middle that become available about 2/3 through the map. I'm worried that on its own the treasure hoard is available too late to matter, but it could be just right for any meta-game rewards that are incorporated later.

The rules have been made more explicit in some cases, and the relic deck has been increased from 16 to 20 cards. The card "Drill Relic" has been replaced - see patch notes for details.

Other Links:

Patch Notes:

I've made some changes to Kudzu's presentation intended to make it scale up more smoothly.

- First, I've split off each dungeon into its own document. Each dungeon module includes the playable map for that level, a guiding layout, and an explanation of spaces found on that map. If there are any cards specifically for that map, they will be included.

- Generic Kudzu material such as rules and cards, however, are only found in a separate document. This way, updating the rules means changing one document instead of several. It also reduces legacy issues with players applying older rules to newer versions of the game.

- The card "Drill Relic" has been removed from the game for now. Having the ability to place tiles on walls is exciting, but has the potential to ruin any map where a major barrier is a single wall thick, as in Lock and Key. Cards with wall-breaking abilities will appear later, but attached to specific maps as starter cards.

Other thoughts and plans: